GSTR-1 Demystified | Tally training in chandigarh

GST brings the idea of transferring business exchange information versus the current

arrangement of recording rundown data. GSTR-1 alludes to recording of outward supply points

of interest by a consistent merchant enrolled in GST at the very latest tenth of resulting month.

These points of interest get auto-populated to counterparty (purchaser) as GSTR-2A on

eleventh. Adherence to dates is of prime significance since separated from late charges (Rs 100

every day up to a most extreme of Rs 5,000), missing due dates prompts changes consequently

recording stream. Idea of return correction has been discarded and changes if any must be

done at receipt level.

Return might be documented by client in following strategies:

Enter receipt information specifically in GST entry – requires rapid and dependable web

availability and appropriate for independent venture. Ex: 50 to 100 solicitations for every month

Enter information in Excel layout gave by GST >> import into disconnected utility >> change

over to uploadable document (.json) >> Login to GST entryway, peruse and transfer – multi-step

process, reasonable for business keeping up information in Excel or utilizing charging or Point

of Sale arrangements (not incorporated with GST) which can give exceed expectations

yield/rundown

associated arrangement: advantageous and favored strategy for most business, as the ERP

would deal with a large portion of the backend exercises (transfer/download/session) with

insignificant physical nearness of proprietor required.

Foremost classifications of data to be outfitted as a component of GSTR-1 may be:

· Sales (Local/Interstate, Taxable/Exempt/Nil Rate, B2B and B2C)

· Exports

· Debit and Credit notes

· Advances

· Revisions for prior duty period

· Other Info (Turnover, HSN Summary, Invoice arrangement and so forth.)

The following is the table-wise points of interest of data to be outfitted:

1. GSTIN – The 15 digit GST Registration number of the business element Ex: 27ARETY3456J1Z1

2(a). Lawful name of the business Ex: One97 Communications

(b). Exchange name of the business Ex: Paytm

3(a). Turnover of past monetary year (2016-17)

(b). Turnover of April-May-June 2017

Total turnover here alludes to consolidated turnover crosswise over India for the PAN, and

incorporates absolved supplies and fares. This does exclude internal supplies on which assess

is paid on switch charge premise.

4. Assessable outward supplies to enlisted business

Assessable supplies are to be accounted for in Table 4 (A to C) and consequently this table

does exclude points of interest of provisions of Nil Rated/Exempt or non-GST products

regardless of whether provided to B2B client. Be that as it may if a receipt has no less than one

assessable thing/benefit it will be accounted for here albeit different things might be

Nil/absolved. Supplies done to SEZ or SEZ designer and offers of esteemed fare nature in spite

of the fact that of assessable and B2B nature won't take part in Table 4. Over all tables when

4A. Outward supplies to enrolled business

Clarification: Taxable deals done to business (B2B) clients having GSTIN and such

administration isn't delegated invert charge. Does exclude B2B deals done through internet

business administrators.

4B.Outward supplies drawing backward charge

Clarification: Sales done to business (B2B) clients having GSTIN of those administrations

named invert charge. Ex: Goods Transport Agency administrations, Legal administrations,

Rent-a-taxicab administrations and so forth.

4C. Outward supplies made through internet business administrators

Clarification: Sales done to business (B2B) clients having GSTIN however done through web

based business administrators like Amazon, Flipkart, eBay, Indiamart and so forth. Deals must

be given isolated web based business administrator astute.

5. Assessable Inter-state B2C supplies more than Rs.2.5 lakhs

Just assessable supplies will be accounted for in this table. (All offers of Nil Rated/Exempt

/Non-GST products or administration to interstate shoppers won't take an interest here).

5A. Between state B2C supplies more than Rs.2.5 lakhs

Clarification: Interstate deals done to buyers (B2C) and the receipt esteem is more than Rs 2.5

Lakhs (does exclude deals done through online business administrator).

5B. Between state B2C supplies more than Rs.2.5 lakhs through internet business administrators

Clarification: Interstate deals done to shoppers (B2C) and the receipt esteem is more than Rs

2.5 Lakhs and the deal has occurred through online business administrators (to be accounted

for internet business administrator shrewd)

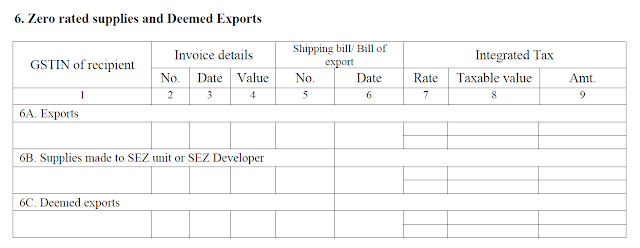

6. Zero evaluated supplies and Deemed Exports

6A. Fares

Fares with or without installment (under Bond or letter of undertaking) of assessment will be

accounted for in this segment. The Shipping Bill number (13 digit code including six digits of

port code) isn't compulsory amid sparing of receipt and can be along these lines refreshed

through alteration table. Transportation charge number is to be compulsorily refreshed before

asserting discount.

6B. Supply to SEZ

Like Exports, supplies to SEZ is zero appraised and can be with or without installment of

assessment, to be accounted for here. Delivery charge subtle elements will be relevant when

provided under Bill of Entry.

6C. Regarded sends out

Regarded sends out as advised by government to be accounted for here.

Cbitss provide Management training and accounting software training , Quickbooks ,

Advance excel And Tally training in chandigarh More detail visit our website and

coll us now - (+91) 9988741983

Advance excel And Tally training in chandigarh More detail visit our website and

coll us now - (+91) 9988741983

Subscribe by Email

Follow Updates Articles from This Blog via Email

No Comments